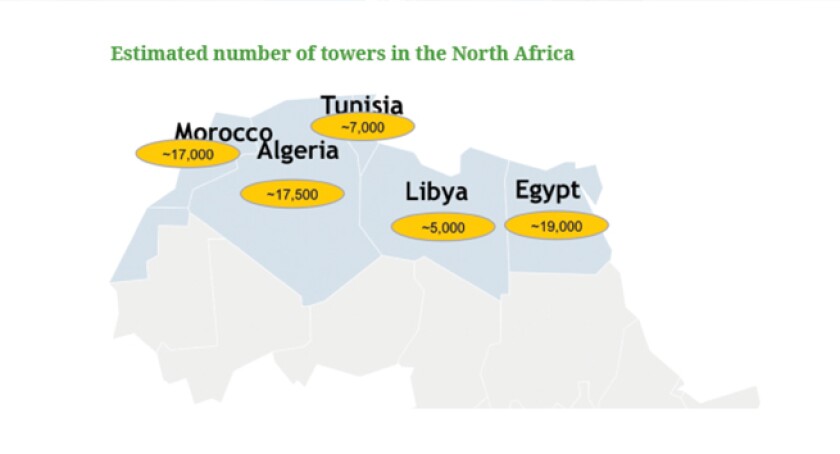

North Africa is a sizeable market, which boasts a number of leading international players such as Vodafone, Orange, Etisalat, Ooredoo and Zain. Unfortunately, with the exception of a potential deal in Egypt, there have not been any other passive infrastructure transactions in the region. While there are merits for passive infrastructure transactions, in the last three to five years, North African operators have had to focus on other more pressing issues such as the Arab Spring or dealings with the government or regulator. However, we are starting to see some light at the end of the tunnel, with ROIC optimisation and increasing 3G/4G investment needs and take up driving the passive infrastructure transactions discussion between operators.

Is North Africa the new hotspot?