Changes to telecoms regulations and market conditions in the past year will impact the towers market in India in various ways. Weighing the positive impacts of 3G and 4G proliferation against the risks of evolving telecom regulation, we believe that growth prospects for towers market are bright, with greater opportunity in diversification into other areas of mobile network support.

Consolidation and advanced mobile networks

The pressing need for operators to establish scale in order to rationalise investments into advanced networks and services has spurred rampant consolidation in the private telecoms sector. If the motive of the M&A is to liberalise the target company’s spectrum holdings and integrate the operators’ networks, then the number of mobile sites in demand will diminish. However, as we believe acquisition targets will be smaller players with limited geographical footprint and financial capability, the risk to tower companies will not be too great. A few recent examples are Reliance Communications’ forthcoming mergers with SSTL and Aircel, and Bharti Airtel’s acquisition of spectrum from broadband wireless access (BWA) operator Augere Wireless.

Conversely, major long-term tenants will be rolling out advanced mobile networks to capitalise on rising smartphone affordability and demand for broadband connectivity, which will improve sharing revenues and tenancy ratios.

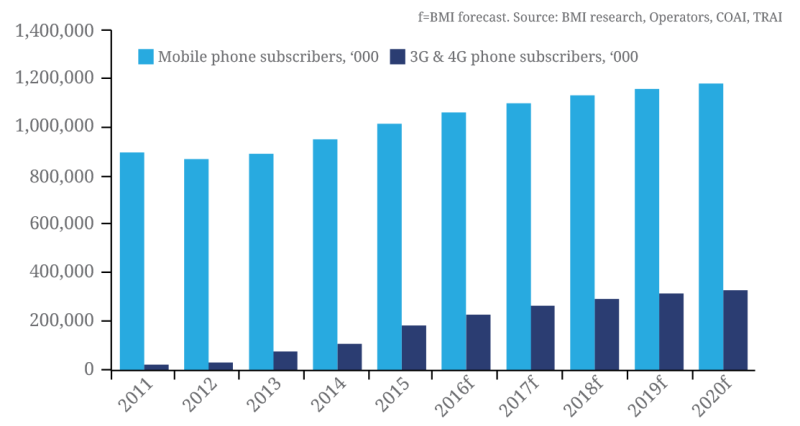

3G and 4G networks, a major source of growth for the Indian towers sector, are being rolled out aggressively as operators seek to recoup their investments in spectrum. The speed of 3G/4G rollouts is also driven by factors such as anticipated demand, operators’ strategies, and heated competition resulting from market consolidation. According to the Department of Communications (DoT), operators rolled out 14,751 3G sites in H215. One such factor driving demand is Prime Minister Modi’s ‘Make in India’ campaign, which will expect to compress the average selling price (ASP) of smartphones - the most popular device for internet access. Market leader Bharti Airtel increased its number of 3G sites by 85.3% in 2015, a growth rate which we believe can be sustained at least into the medium term and will be the key upside to towers’ lease rates and tenancy ratios.

We forecast strong 3G/4G subscription growth of 85.6% in our current five-year forecast period, from 173.7mn at end-2015 to 322.3mn by end-2020. While this growth rate factors in the positive effects of operators’ subsidised data and smartphone bundles, as well as the rising middle class, we highlight that our end-2020 forecast figure represents a population penetration of just 23.2%. Keeping in mind that initial rollouts are focused on the wealthier and more densely populated and urban cities, this means there is still plenty of room for 2G to 3G/4G subscriber migration to take place through the medium-to-long-term, particularly from rural regions.

BMI is bullish on growth in 3G/4G and the ICT industry for several reasons. Firstly, India outperforms the region in real GDP growth, which our Country Risk team forecasts to reach 7.2% in FY2016-2017 (year-ending March). In particular, we are bullish on the country’s manufacturing and services sectors, to which the aforementioned ‘Make in India’ initiative plays an integral role. India also continues to implement Pro-business reforms, as exemplified in the government’s FY2016/17 union budget for corporate tax rates for small enterprises (with turnover less than INR50mn in FY2014/15) and new manufacturing companies (incorporated on or after March 1) to be lowered to 29.0% and 25.0%, respectively (from 30.0%), while start-ups set up from April 2016 to March 2019 will enjoy tax exemptions.

Regulatory developments: Spectrum, active infrastructure and network sharing guidelines

India’s telecoms sector has witnessed a series of regulatory reforms led by the Telecoms Regulatory Authority of India (TRAI) and the DoT that, we believe, could further accelerate the speed of 3G and 4G network rollouts.

Recently implemented active infrastructure and spectrum sharing guidelines mean that entering into such sharing agreements could eliminate the need for operators to have their own transmission equipment such as antennas and Node B in areas where they are sharing spectrum, reducing the number of operators demanding tower sites and consequently, the potential sharing revenue tower companies could gain.

The DoT has also recently approved regulations that will allow Mobile Virtual Network Operators (MVNOs) to launch in the market. While we believe current market conditions leave MVNOs little room to make a substantial impact, there will be no lack of interest from companies hoping to establish new verticals by entering the mobile business.

Small-scale mobile operators, being able to gain from spectrum monetisation, will be able to broaden their network sites in circles where they hold spectrum. For example, Videocon, a minor operator with just a 0.7% market share, recently disclosed plans to purchase new 2,100MHz 3G spectrum in Punjab with the INR44.28bn it received from selling its 1,800MHz 4G spectrum to Airtel earlier this month. Revenue-sharing agreements with MVNOs and more efficient spectrum utilisation will incentivise such operators to raise their site counts to optimise network coverage.

Xiaomi, for one, could be interested in this prospect to boost its value proposition in India. Leveraging its experience of operating as an MVNO in China, the smartphone manufacturer’s recent US$25mn investment in local online content publisher Hungama Digital Media Entertainment suggests that the company is hoping to pursue more than a hardware strategy, adding to its footing in the Indian market. By bundling telecom services together with mobile devices and value-added services, companies such as Xiaomi can provide competitively-priced packages and build customer loyalty.

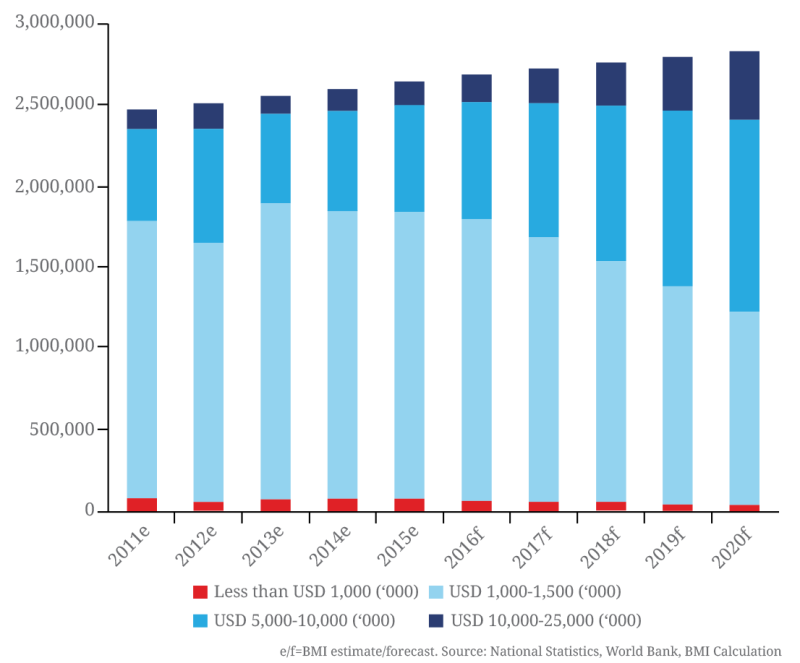

Rising middle class to lift 3G/4G adoption

India - household income (2014-2020)

Competition and opportunities in services

The government’s instructions for operators to address the prevailing call drop issue could improve tenancy ratios and lease rates in new areas. Noida district’s Mobile Tower Installation Policy-2013, for example, previously banned telecoms towers from being situated in residential areas, but was revised following the DoT’s guidelines. Private operators were mandated by the DoT to install 29,000 new mobile towers, while BSNL installed 4,500 and MTNL installed 28 in Delhi. As investments into advanced services continue to force towers that are still held operator-captive to be released into the market, we believe that directives to address telecoms quality of service (QoS) issues will translate to a booming towers market.

A new minor risk to tower companies in India is the rise of independent players, such as Facebook through its Express Wi-Fi project, which are building up their own custom networks and infrastructure in the country. However, this is limited to rural regions where lease rates and tenancy ratios are generally lower, and will not eliminate the need for traditional telecoms towers which can be better adapted to evolving technological trends.

We believe these changes in the telecoms sector could impact the nature of towers companies as well. While the changing regulatory landscape could be interpreted as a boon for mobile operators, but a bane for the tower industry, we highlight the opportunity for tower companies to leverage heavy mobile network traffic to diversify their businesses in anticipation of growing demand for fibre backhaul and small cell network solutions.

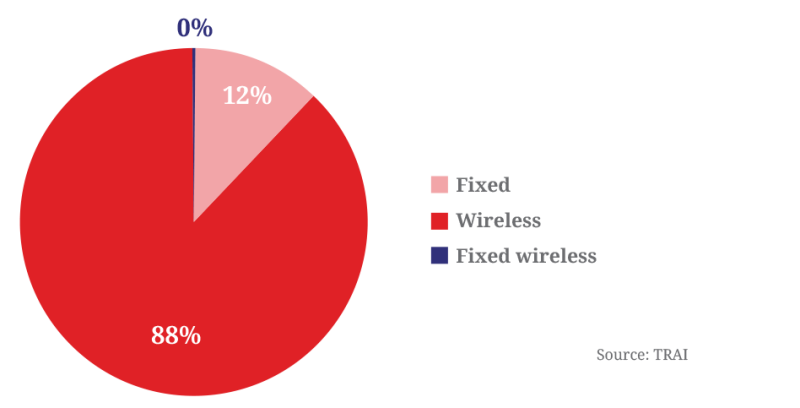

Mobile towers play key role in national broadband connectivity

India’s broadband subscriber market (Q415)

Revenue growth prospects avail

Bharti Infratel - key operating metrics (Q312-Q415)