Mobile market overview

Algeria had an estimated population of 40.0mn people and 45.4mn mobile subscriptions at the end of 2015, giving a mobile penetration of 113% - the second lowest level of penetration of the six North African countries, only higher than Egypt (101%). Around 90% of subscribers in Algeria have a pre-paid account, which ranks second lowest amongst the North African countries.

There are three Mobile Network Operators (MNOs) serving the Algerian market, each holding a substantial share of the subscriber base. Djezzy currently holds the largest market share with 17.0mn subscribers closely followed by Mobilis (Algerie Telecom) with 15.3mn and Ooredoo (NMTC) who serve 13.0mn subscribers.

Key mobile developments

Algeria’s mobile subscriber base has grown rapidly in recent years, increasing by just less than 30mn in the last 10 years. Estimates suggest that the increase will begin to slow marginally with the subscriber base expected to reach 52.5mn in 2020.

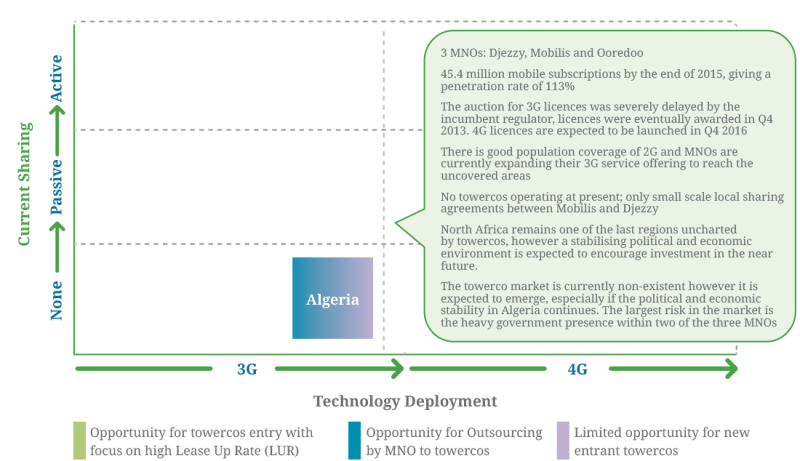

The tender for 3G licences was first announced in Algeria in Q2 2008, however it took until Q4 2013 for the auction to take place and the licences to be awarded. Postponements were reportedly due to the Algerian government completing the acquisition of local mobile operator Djezzy. The three main operators, Djezzy, Mobilis and Ooredoo, all successfully acquired licenses through the auction process and began to roll-out their 3G service offerings almost immediately. By March 2014, Ooredoo had extended its network to reach 70% of the population which provided the operator with a commanding 71.7% share of the market. As the other two operators established their 3G networks they quickly eroded the market share of Ooredoo - culminating in the market share split shown above.

Developments in 4G

In January 2016, the Algerian regulatory authority (Autorite de Regulation de la Poste et des Telecoms, ARPT) invited interested parties to submit proposals for participation in the country’s 4G auction. Successful bidders are expected to be notified in May 2016 with the launch of the licences officially taking place in Q4 2016. A stipulation attached to the purchase of the 4G licences is believed to be expansion into the Southern regions of the country within the first three years.

Algeria is generally in line with the 4G developments of its North African neighbours. The Tunisian regulatory authority has accepted proposals for 4G licences which are expected to be allocated in April 2016, the Sudanese regulatory authority awarded its first 4G licence to MNO Zain in February 2016 and reportedly the most advanced 4G market in North Africa is Morocco where all three incumbent MNOs were granted 4G licences at auction in March 2015. Egypt and Libya are reportedly less advanced in the roll-out of 4G services however promising regulatory and market activities have been observed.

Operator activity

Mobilis (Algerie Telecom) is a subsidiary of the fixed telephony, internet and satellite communications provider Algerie Telecom which is solely owned by the Algerian government. In a bid for independence Mobilis unveiled plans in 2015 to acquire its own fibre optic network infrastructure which has caused a dispute with its parent company which currently provides Mobilis with fibre capacity on its own infrastructure. Orange and Vodafone have expressed interest in acquiring a stake in Mobilis in recent years, however reports suggest that a listing of a 20% stake of Mobilis on the Algiers Stock Exchange is most likely.

In Q1 2015 the Algerian government purchased a 51% stake in Djezzy from Global Telecom Holding (GTH), a holding company of the Russian-backed VimpelCom group. GTH maintains a 45.57% share and the remaining 3.43% is owned by private conglomerate Cevital. In Q4 2014 Djezzy commissioned Alcatel-Lucent to upgrade its GSM network, using a microwave solution to upgrade its backhaul architecture.

Ooredoo rebranded from Nedjma in 2013 and is part of the Kuwait based Ooredoo Group. Ooredoo is the smallest operator in Algeria by total market share, however it sits very closely behind market leader Mobilis when considering the number of 3G subscribers, 6.1mn to 6.7mn subscribers respectively. In 2014, Ooredoo and Alcatel-Lucent built a 400Gbps backbone in order to support the country’s growing 3G market and in order to deliver improved speeds and capacity to Algeria’s main towns and cities.

Mobile subscriptions- market share

Regulation

ARPT is an independent institution with separate legal and financial operations from the Algerian government. ARPT oversees a number of postal and telecommunication matters, including spectrum licensing, promoting competition, dispute resolution and supply regulation.

Although ARPT is managed separately from the Algerian government, instances have been reported which suggest cooperation between the two parties. The most noticeable of these instances was the five year delay in auctioning the 3G licences which caused significant frustration for the incumbent mobile operators. The delay is reported to have been due to the 51% stake acquisition by the Algerian government of the MNO Djezzy.

ARPT is governed by a board and designated CEO which are chosen by the Algerian President. The board is provided with the powers required to manage its operations and the board uses a majority voting system where the Chairman has the casting vote.

The tower sharing market

North Africa remains one of the last regions uncharted by towercos. Reports suggest that instances of political instability, such as the Arab Spring in 2011, and unpredictable regulatory involvement have caused investors to stay away from the region to date. Analysts advise that as the region stabilises politically and economically, the countries will benefit from improved outsourcing readiness and more passive infrastructure deals are expected. Algeria follows the same trend as the other North African countries and the estimated 17,500 towers in Algeria currently belong to the three operators.

Although independently managed tower sharing is yet to develop within Algeria, Mobilis and Djezzy signed a sharing agreement in Q1 2014 with the main aims reported to be a reduction in environmental impacts and expenditure whilst improving the network coverage of both operators across the country. This sharing agreement came less than six months after an agreement was signed by Mobilis with the tower construction company Tubprofil to erect future towers on Mobilis’ behalf.

Conclusions

With the second highest population in North Africa (40.0mn people) and one of the lowest mobile penetrations (113%), there is considerable room for subscriber growth in the Algerian mobile market. There is a good population coverage of 2G and the incumbent MNOs have recently been authorised to complete the roll-out of 3G services to the remaining uncovered areas of the country. To date, Algeria has matched the technology developments of the other countries within the region with 4G licenses expected to be awarded to successful bidders by the end of 2016.

The three MNOs have a similar market share which encourages competition. The three MNOs all successfully acquired 3G licences and are reported to have submitted proposals for 4G licences which will help to ensure a continuation of competitive pricing within the market. Concerns have been raised about the regulatory authority’s involvement and influence within the market in recent years, especially considering the links with the Algerian government and its financial interest in two of the three MNOs (Mobilis and Djezzy).

Algeria has a good 2G population coverage and a largely developed 3G coverage, however the mobile penetration remains relatively low for the region which would suggest a suitable environment for growth. As the growth potential is realised, future rollout is expected to be largely driven by 4G deployments and expansion. In combination with stabilising political and economic conditions, the Algerian market is expected to entice passive infrastructure investment in the near future.