At the 2017 TowerXchange Meetup Africa, we were delighted to welcome three heavy weight MNOs to the stage. MTN were represented on the panel by Group CTO, Navi Naidoo. The operator, with a footprint in 20 countries, is Africa’s largest MNO and has divested towers in seven of its markets (see figure one). Orange were represented on the panel by Nat-Sy Missamou who heads up the operator’s infrastructure sharing initiatives, managing relationships with towercos as well driving their exploration of the ESCO market. Etisalat were represented by Wiktor Barcicki who oversees technology economics for the international unit of the operator, supporting the different opcos in spending capex and opex more efficiently whilst providing input into special initiatives such as infrastructure sharing and tower deals. The panel was moderated by Darragh Stokes, Managing Partner of Hardiman Telecommunications.

How strategy is set market to market

With each of the invited panellists sitting at group level within their respective company, the question arose as to what extent passive infrastructure strategy was driven by the group level and to what extent it came from within each opco. Orange explained that strategy was driven heavily by head office in Paris, although market and cultural differences meant that the company’s opcos were broadly divided up into different clusters with common strategies. This pattern was very much echoed by MTN who ran the strategy centrally but with regional groupings and different tiers of operations. For Etisalat there was very much a combination between group and opco-led strategy; with the Maroc Telecom-owned opcos having, to date, operated rather independently, although Etisalat is looking to become more closely involved.

Whilst group level may be involved in setting strategy, strategy is not homogenous across all opcos in an operator’s portfolio. The macrodynamics in a given country heavily affect an opco’s spending, and so too does the opco’s time of entrance and market share. Where an operator is number one in a market, they will have a very different strategy to one where they are sitting in a much lower position. Speaking on the Kenyan market, Orange referenced how they had made the decision to exit the country as they were never going to be able to topple Safaricom from their number one spot; in the DRC, however, the company is making significant headway in growing their market share. On the subject of time of entrance into a given market, Etisalat explained how their late entrance into Nigeria had been a contributing factor to their struggles in the country, although a crashing economy and currency devaluation were the main factors that led to their eventual exit.

Prioritisation of investment in spectrum and active infrastructure

The MNOs commented on how demand for connectivity is outstripping capacity across the region; it being particularly surprising how rapidly data usage is growing, in spite of the low smartphone penetration in much of sub-Saharan Africa. This particular issue of data usage growing whilst smartphone penetration remains low presents a key problem to operators on the continent; they need to maintain 2G networks to support older handset users whilst also rolling out 3G and 4G to meet the growing data usage by others. Whilst in some parts of Europe and Asia, 2G has started to be switched off, it isn’t possible to do this in Africa as you cut off a large subscriber base. Today’s operators need to add 3G, LTE and U900 as well as 2G to towers thus creating significant capex and leasing costs.

Requirements to continually rollout and use multiple technologies simultaneously not only puts a strain on budget but also on spectrum usage, with access to additional spectrum presenting another key problem to the region’s MNOs. In particular, one of the operators on the panel voiced their struggles in obtaining the lower band 700MHz and 800MHz spectrum; spectrum critical to getting inside buildings and being able to offer high speeds. Without access to adequate 700MHz and 800MHz spectrum, capex outlays can quickly escalate when trying to improve connectivity.

As such, the operators explained how it was of critical importance to work closely with OEMs to get the most out of their spectrum, whilst working closely with infrastructure providers to reduce the costs of rolling out new sites. Early discussions on the panel reinforced the well established viewpoint that operators have a preference for focussing investment on active equipment and spectrum, whilst finding ways to reduce their spend in other areas.

In markets where revenues were dependent on the 2G voice segment, due to a lack of 3G and 4G handsets in use, operators were keen to drive data usage, transitioning users from 2G to 3G and increasing ARPU and customer experience. On the other hand, Etisalat explained that in a significant proportion of their markets, LTE coverage was well over 90% and as such the focus there remained about improving capacity rather than improving coverage. The Middle East, where Etisalat has a significant footprint, has some of the highest data usage figures globally, figures which are continuing to climb.

Whilst there was a preference to spend on spectrum, active equipment and services, operators were also focussed on deploying capex on making the network more efficient; consolidation of infrastructure, cloudification of platforms and bringing multiple countries into a “common factory” remained a key focus at Etisalat.

Infrastructure sharing and the role of towercos

Infrastructure sharing is, of course, one key methodology to make networks more efficient. When questioned as to what extent they view their networks as a differentiator and to what extent they were willing to share, the panellists explained that it was important to include a “timeframe” parameter in the question. When you are the first to roll out infrastructure in a given region you benefit from a first mover advantage; whilst you are securing market share during this period there is less of an appetite to share. After 12-18 months most of the first mover advantage has been obtained and, as such, operators became more willing to share as a means to reduce costs.

Where the MNOs have entered into towerco agreements or passive infrastructure sharing agreements with their competitors was to some extent influenced by the different markets in which they were operating. Orange explained how in Central and Eastern Africa there was a good presence of towercos and so they tended to use them to rollout and manage their passive infrastructure; conversely in West Africa there was a limited amount of towerco activity in many of the operators’ markets thus limiting their use. Additionally, in West Africa there is less of a culture of infrastructure sharing between operators which has also limited Orange’s strategy on this front; in North Africa however, operators tend to be much more open to infrastructure sharing - an attitude which could ultimately make active sharing a possibility.

MTN has divested their towers in seven markets (see figure one); these divestments represent the majority of the most attractive markets to towercos with some markets where they still retain towers being too small to attract the interest of the major players. MTN explained, however, that they continue to evaluate their strategy in relation to tower sales, assessing what is best for them in each region. On the subject of giving build to suit contracts to towercos, MTN explained how this was dependent on a number of different factors. There may be times of year when the opco is particularly capex constrained and thus in these instances contracts may be given to towercos. At the same time, it depends on whether towercos can offer the most competitive price relative to other vendors, with this not always being the case.

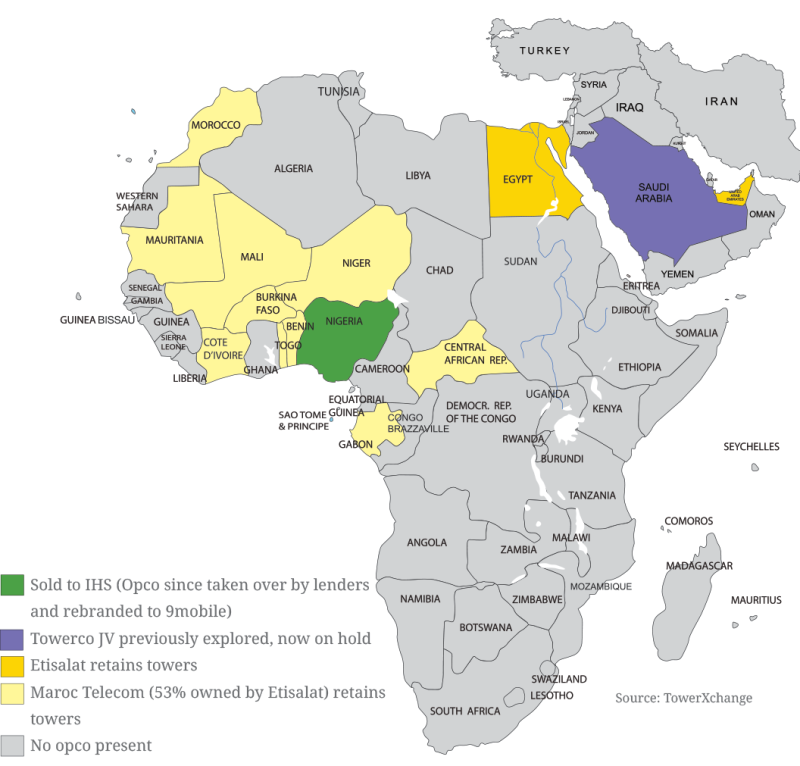

Etisalat explained that increasing the utilisation of both their passive and active infrastructure is an essential part of the company’s strategy to lower their cost base. To date, the adoption of infrastructure sharing has been lower than they would like, with many agreements having taken a long time to reach. The lack of regulatory frameworks regarding infrastructure sharing has been a contributing factor to these delays, with there being a difficult decision as to whether you should wait for the frameworks to be ironed out and lose out on benefits in this time; or alternatively forge ahead but potentially risk penalties down the line. Etisalat now have some degree of passive infrastructure sharing in the majority of its markets, working with other MNOs to look at deeper cooperation, although regulatory challenges can prevent active sharing from being feasible. Etisalat has more limited experience in working with towercos, having only sold towers in Nigeria, a market which the towerco has now exited. The company’s Saudi Arabian opco, Mobily, had previously explored a tower sale only to cancel it to explore the formation of a joint venture with Saudi Telecom Company, with plans for the joint venture also now on hold (see figure three).

Figure one: MTN’s footprint and history of tower sales

Figure two: Orange’s MEA footprint and history of tower sales

Figure three: Etisalat’s MEA footprint and history of tower sales

Experiences working with towercos

On the subject of how positive their experience working with towercos has been, each of the MNOs explained that it has not always been plain sailing. Lessons have been learned along the way and there is need to constantly be in discussions and negotiations. Inflation linked contracts, exposure to forex issues plus concerns with power cost and availability have all presented challenges in MNO-towerco relations. In addition to this, operators cited examples of advantages being given to their competitors, in terms of both pricing and access to sites, which has put a strain on relationships.

Another challenge faced by divesting tower portfolios to towercos comes when an operator needs to roll out sites to areas in which towercos do not want to build. With the towerco business model being predicated on securing multiple tenants, and lease payments being their source of revenue, there are areas which are unattractive for a towerco to enter. For operators who have outsourced passive infrastructure, this presents a challenge as they have lost a large proportion of their in house capabilities to build and manage towers.

In spite of this, MNOs did confirm that on the whole, the quality of their networks has improved when they have passed on their towers to towercos. An operator is less incentivised to want to spend money on purchasing the highest quality energy equipment, preferring instead to invest heavily on active equipment. For a towerco, energy equipment is their “active equipment” and so the focus and spending that they have placed on this has delivered results.

The potential held by ESCOs

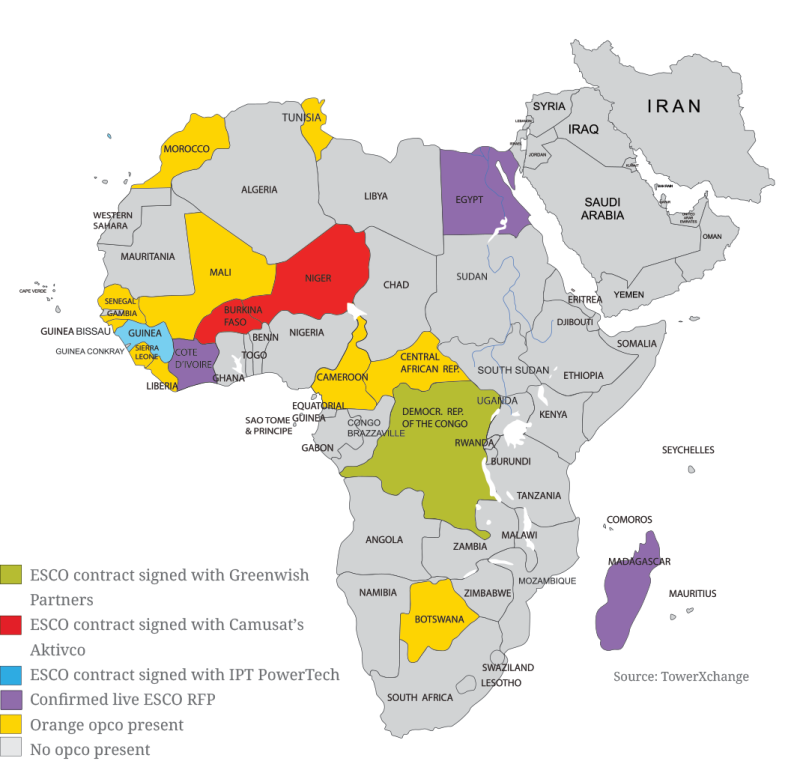

With outsourcing to towercos having delivered improved power uptime, discussion turned to the role that ESCOs could play in each of the operators’ networks. Orange are the most advanced in terms of studying the ESCO model, having signed contracts in the DRC (with GreenWish Partners), Guinea Conakry (with IPT PowerTech) and Niger and Burkina Faso (with Camusat’s Aktivco) – see figure four. Whilst it was perhaps too early to comment on the impact of ESCOs, Orange expected similar benefits to be observed as had been when outsourcing to towercos. With energy equipment being an ESCO’s number one priority in terms of deploying capex, one would expect that similar improvements in power uptime would be seen when sites were taken over by ESCOs.

MTN is just at the beginning of their path in exploring the suitability of ESCO contracts, but for markets where the operator does not expect to sell their towers, the ESCO model could offer an attractive alternative. Etisalat explained that they are not actively looking at the ESCO model at present although they may start to explore this more in a few years. For now, their focus remains much more on improving energy efficiency through the deployment of batteries and cooling solutions.

Figure four: Orange’s exploration of the ESCO model

The next TowerXchange Meetup Africa & Middle East will be held on 9-10 October 2018 at the Sandton Convention Centre Johannesburg. For more information please click here.