Cellnex Telecom and BT have signed a long-term strategic agreement worth £100mn, allowing Cellnex the rights to operate and market 220 high towers owned by BT for the next 20 years. The agreement sees Cellnex increase the total amount of telecom sites it manages in the UK by almost 40%. Cellnex will manage the existing service contracts for these sites and offer new equipment co-location services. Both companies will share the additional revenue streams that are expected to be generated. Cellnex and BT are committed to exploring the potential for further collaborative opportunities.

TowerXchange: Congratulations on the announcement of your partnership with BT, securing the marketing and operating rights for 220 high towers in the UK! This seems like a unique kind of deal, so let me ask first what is the difference between these 220 high towers and conventional mobile masts, in terms of the structure of those sites, the original intent for which they were built, their location, and the potential to lease them up to multiple tenants?

Ester F. Montorio, UK Country Manager, Cellnex:

This tower portfolio is one of BT’s historical portfolio of sites. The high towers have been used over the years mainly to host broadcasting and transmission services, and are now being used to co-locate MNOs’ networks. The idea is to revamp the use of these towers to host new services such as 5G and other innovative network solutions for telcos.

TowerXchange: I note that Cellnex and BT will “share additional revenue streams” generated from the partnership. Can you share more colour on the deal structure? It doesn’t sound like a traditional sale and leaseback – is it more akin to a manage with license to lease deal, or something entirely unique?

Ester F. Montorio, UK Country Manager, Cellnex:

The structure of the deal proposes a unique and different approach, which is consistent with the fact that we are not speaking about assets acquisition, but about exclusive marketing and operation rights of those assets and for a long period of time.

In fact this structure reflects the underlying ambition of this deal, which is fixing the fundamentals for a long strategic partnership with BT in the UK. Co-operation among different players in the value chain of the telecom networks will become increasingly critical and strategic to achieving the challenging targets ahead of us like the 5G roll-out. Agreements between telecom operators like BT and telecom infrastructure neutral host operators like Cellnex, will be an important part of bringing the benefits of breakthrough technologies like 5G to as many parts of the geography as possible.

For Cellnex, this deal is a landmark first step into the UK market and follows our recent successful acquisitions of 10,700 sites from Iliad and Salt as well as a strong set of Q1 results. This agreement demonstrates the Company’s commitment and confidence in the market as we look ahead to further opportunities in the UK” – Alex Mestre, Global Business Managing Director, Cellnex

TowerXchange: Can we put this partnership into the context both of Cellnex’s existing portfolio in the UK, primarily traced back to the acquisition of Shere Group – what assets do you have, and what magnitude of revenue are you generating in the UK?

Ester F. Montorio, UK Country Manager, Cellnex:

Right now and after this new agreement with BT, Cellnex UK will operate more than 820 sites and towers in the UK. Roughly speaking this means that we have increased our infrastructure capabilities around 40%.

Clearly speaking the agreement achieved is both akin of a small “quantum leap” for us in the UK market since the Shere Group assets acquisition in 2016, and a confirmation of our commitment to playing a role in the British telecoms market. Bearing in mind the UK projects pipeline that we are currently exploring, we are convinced that our presence as a significant player will further increase. We fully appreciate that the British telecoms market is one of the biggest and more dynamic markets in Europe and, as our scope is a European one, this fits completely within our strategy.

TowerXchange: Can we put this deal into the context of Cellnex’s future ambitions in the UK? The UK is a uniquely structured tower market, with ~31,000 cell sites operated by Cornerstone (a joint venture between Vodafone and O2) and MBNL (a joint venture between BT and EE), while Arqiva has around 8,000 telecom infrastructure sites. Wireless Infrastructure Group and Cellnex UK are the largest independent towercos, with a handful of sub-thousand tower competitors. How do Cellnex view organic and inorganic growth opportunities in the UK against that backdrop?

Ester F. Montorio, UK Country Manager, Cellnex:

Our long-term vision of the business is to make our businesses grow and provide excellence to our clients. Organic growth is of course our preferred option since we entered the UK market, and as anticipated we are involved in several projects that will see the light soon. We will keep the market updated on these and others that are continuously monitored, as the prospects evolve and opportunities in the transport and indoor coverage segments come to fruition.

Organic and inorganic opportunities are both drivers of our growth strategy. Inorganic growth allows us to increase our scale and dimension, which is important for a telecom passive infrastructure provider. Organic growth tells us about our technology and engineering capabilities that make us an attractive partner in order to play an active role in projects related with the upcoming 5G roll-out. As well as improving the current LTE coverage, our know-how in areas like small cells and DAS deployment, both for outdoor and indoor coverage, fibre connectivity, edge computing, et cetera, will become key elements of the 5G ecosystem. Our experience of combining both organic and inorganic growth is a good formula to make our business grow, while continuously challenging it to keep it on trend.

We are pleased to be working with Cellnex to help bring a more flexible approach to the UK’s site share market. BT and its EE mobile arm recently switched on the UK’s first 5G network across six cities and as the roll-out of 5G continues, agreements such as these will be an important part of bringing the benefits of the technology to as many parts of the country as possible” - Alex Tempest, Managing Director, Wholesale, BT

TowerXchange: Much of the new build in the UK is likely to be densification sites in readiness for 5G, and many such sites will be micro rather than macrocells. Does Cellnex have a view on the merits of the Concession system whereby local councils offer exclusivity in the lease-up of lampposts and other street furniture – particularly in the light of BT returning their concessions?

Ester F. Montorio, UK Country Manager, Cellnex:

We have a view on the current business models that typically govern telecos’ equipment accommodation on street furniture here in the UK. In fact, we have been participating in tender processes in London in the past to this effect. This is an ecosystem where Cellnex can bring fresh insight, as we have experience in managing public furniture in other cities, such as Barcelona, where we use alternative business models to the current ones used here.

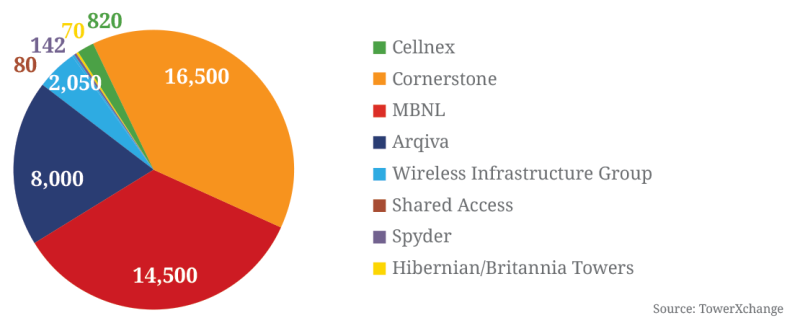

Who owns/operates the UK’s 42,162 active cell sites?

The UK tower market

The UK has a tower market structure unlike any other in the world. Independent towercos, headed by Arqiva, Wireless Infrastructure Group and Cellnex (which acquired by Shere Group in 2016), own 26.5% of the 42,162 active towers in the UK. The balance are contained within two joint venture infracos: Cornerstone, which operates Vodafone and O2’s network (Telefónica), and MBNL, which performs a similar function for EE (now BT) and 3 (Hutchison).

Cornerstone and MBNL are both the primary clients of the UK’s independent towercos, and site sharing businesses in their own right. Their business models differ in that the tower assets are actually on Cornerstone’s balance sheet, while MBNL is a management company with the assets retained by the MNOs. Cornerstone is a passive infrastructure sharing play, while MBNL’s model extends to active infrastructure and transmission sharing.

Recent comments from Vodafone’s senior management suggest that Vodafone and O2 UK are considering their options in terms of monetising Cornerstone. This could result in offering co-locations on Cornerstone infrastructure to third parties beyond Vodafone or O2, or it could relate to the sale of a minority or majority stake in Cornerstone and its ~16,500 UK towers and rooftops, a prospect which has raised the interest of towercos and investors across Europe.

The UK’s broadcast tower operator Arqiva has been through many changes of identity and ownership (BBC, Crown Castle, National Grid to name a few), and was believed to be close to agreeing a sale to a consortium of buyers led by Brookfield in 2017, before a short-lived attempt at an IPO later that same year. It remains to be seen whether Arqiva will revisit the option of a strategic sale or IPO, or give themselves some breathing room to show that their improving EBITDA is sustainable in order to close the gap between their expectations and market valuation.

Analysis of the transaction

Cellnex’s agreement to operate and market 220 high towers owned by BT in the UK paves the way for future long-term co-operation between Cellnex and BT. While amplifying Cellnex’s UK site count to over 820 provides immediate increased scale, the bigger news may be that both companies are committed to exploring joint projects in areas that will be key in rolling out 5G. It remains to be seen exactly how that will play out, especially given that BT / EE’s passive and active infrastructure is operated by MBNL, which has a similar relationship with Three.

Although the path to 5G presents many obstacles, there are clear signs that infrastructure owners are beginning to lay the foundations for roll-out with joint projects and co-operation, and Cellnex and BT stand out as a clear example.

The first phase of 5G roll-out will require that macro networks be reviewed for structural and power capacity, after which we anticipate an increase in the number of infill are being built. In urban areas, MNOs and neutral hosts are working to build relationships with local government, fibre providers and street infrastructure owners in order to secure the real estate needed for larger scale small cell roll-out. Towercos such as Cellnex, Arqiva, Wireless Infrastructure Group and many more are acquiring businesses in adjacent verticals or forming partnerships which will enable them to get ahead once larger scale 5G roll-out takes place.